Posted by Joe Paduda on Wednesday, February 27th, 2019 | Comments

There is no consensus about what MFA is – and that makes it really easy for supporters and opponents to convince the uninformed it is great or awful.

They do that by picking out whatever they think you’ll love/hate – even if it has nothing to do with MFA. Then, they yell about that at maximum volume in an effort to convince you that the whole thing is terrific/awful.

Before we decide if MFA is worse than the stomach flu or better than a teenager that actually listens to mom and dad, let’s spend two minutes understanding what MFA is.

There are three general “versions”, each coming in multiple variations and with different tweaks. The basic differences are:

who is covered

what types of healthcare are included

is there a role for private insurers

what mechanism/payer system is used.

Notably, many of the proposals aren’t exactly precise on where the dollars to pay for all this will come from.

There’s the Bernie Sanders version which is basically – every kind of healthcare service anyone could think of for free for everyone – provided only by the government, with no private insurance allowed. Another even richer version is to be announced today – which is even more generous – and hyper-expensive.

My take – completely unrealistic for several excellent reasons which I’ll get into in a future post.

Then there’s Medicare for some – which would allow older folks to “buy in” to current versions of Medicare, while leaving employer-based insurance alone. A similar proposal, known as the “Public Option” was part of the ACA until the Democrats took it out in an unsuccessful effort to get Republican support for ACA legislation

My take – this makes more sense for multiple reasons; again we’ll dive into this next week.

Some – including your author – have pitched Medicaid for some or all. To me this is more viable as it heavily involves states, wouldn’t affect federal taxes nearly as much as Medicare for All, and uses an already-existing program that is much simpler than Medicare.

What does this mean for you?

A gentle reminder – yes, there are issues with all of these. But what is the alternative? Our current system is a mess and is getting worse by the day. If you object, what’s a better solution?

What does this mean for you?

Change is coming – make darn sure you understand what it means for you.

Posted by Joe Paduda on Tuesday, February 26th, 2019 | Comments

MFA/M4A uses Medicare as the health insurance mechanism for people younger than 65. Some advocates are pitching “Medicare for Some” wherein folks older than 50 or 55 would be able to “buy-in” to Medicare (which covers everyone over 65 today).

Current beneficiaries really like Medicare – more than insureds like private insurance

It relies on an existing system and infrastructure that exist today and are familiar to all stakeholders

Administrative expenses are much lower than employer-sponsored and individual insurance

Price controls are universal and apply to almost all types of providers

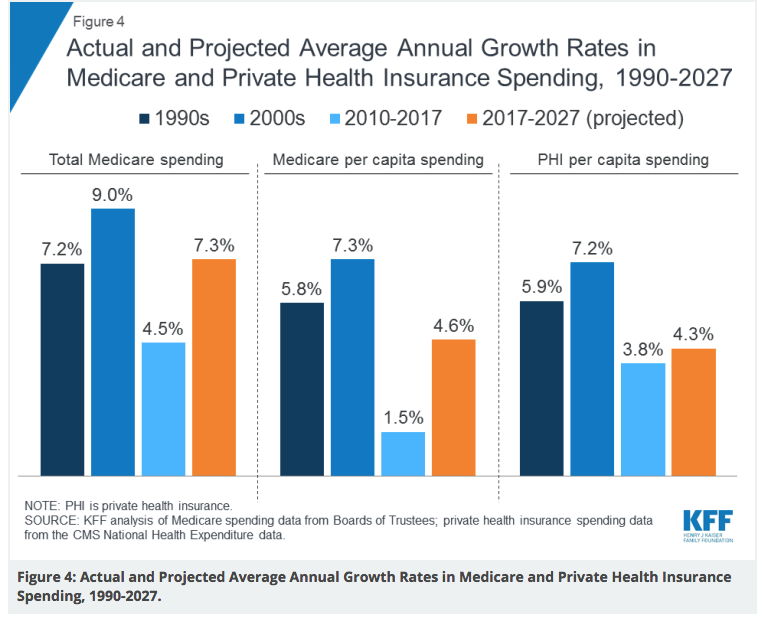

Cost increases – on a per-capita basis – are lower than in commercial health insurance

Pretty much all doctors and hospitals accept Medicare

Commercial insurers are very active in Medicare, offering plans that provide added benefits for little to no additional cost (however there are usually limits on providers patients can use (known as Medicare Advantage plans)

Those who like “traditional” Medicare can buy supplemental benefits from private insurers to cover services, deductibles, copays and other costs not covered by Medicare (Medicare Supplement plans)

Opponents cite:

It would be wildly expensive and require massive new taxes, with annual cost estimates ranging from $1.4 to $2.8 trillion (although one major opponent concedes total US healthcare costs would be $2 trillion less a decade into MFA)

Medicare reimbursement is too low, forcing providers to upcharge other payers to make up for lost revenue. If Medicare is the only insurance carrier, then providers will be in dire financial straits.

People covered by employer-funded health insurance are leery of losing those plans.

The notion of “government-run” healthcare scares some, but most don’t even know Medicare IS a “government-run” program.

My take

There’s no question Medicare is less expensive than group/individual health insurance – and costs will increase more slowly. Private insurers are heavily invested in the business, so they can handle the admin piece. Yes, taxes would go up, but employers’ costs would likely drop considerably. Patient hassles would greatly diminish.

Oh, and given what a pain in the butt commercial insurers can be when it comes to out of area coverage, deductibles, annual premium increases, covered v non-covered services and everything else they do to make our lives miserable, I’d be way happier with Medicare for me and my wonderful bride.

Posted by Joe Paduda on Monday, February 25th, 2019 | Comments

You’re going to hear a lot about Single Payer over the next 20 months – mostly from people who a) have an opinion about it and b) don’t even know what “Single Payer” is.

Before you get sucked into that discussion/argument, here’s a primer.

“Single Payer” – by definition – is government-financed and government-managed health insurance.

Beyond that, pretty much every country with Single Payer is unique, each with its own nuances. For example,

most don’t have government-employed healthcare providers; in many single payer systems, physicians, therapists, hospitals and other providers are private.

The UK is an exception; providers are (mostly) employed by the government

many are not government-operated; in many systems private insurers contract with the government to handle administration of health insurance – similar to our Medicare

Again the UK is an exception

Typically:

the government sets pricing/reimbursement policy and actual prices – similar to our Medicare

funding comes from some combination of employee, employer, and other taxes; in some countries, insureds pay some form of premiums – similar to our Medicare

it covers everyone

there is little to no paperwork for patients/consumers; all that is handled by the administrative agency

there are minimal or no deductibles, copays, or co-insurance requirements

people can buy into supplemental insurance through private insurers

What does this mean for you?

You are now more knowledgeable than most everyone else about Single Payer.

Here’s what One Call is doing to, at least partially, address the debt situation. First, recall that OneCall has about $2 billion in debt outstanding. The company appears to be working to reduce its debt expense – the interest payments that amount to somewhere around $150 million annually.

There are two parts to this debt restructuring. Simply put, One Call is doing two things – in both cases asking current debt holders to swap their existing notes for new ones. In both cases One Call has structured the new debt to allow the company to not pay interest if it chooses.

The mechanism One Call is using isn’t that unusual, it’s known as “PIK toggle” loans; “Payment In Kind toggle” notes allow the issuer to forgo interest payments by giving debt holders more first-lien notes instead of paying the interest due in cash.

Got that? I know, complicated stuff.

Here are the details.

Part one

According to Bloomberg, after dropping its previous debt exchange effort One Call offered debt holders “sweeter terms” on a revised deal allowing “certain first and second-lien creditors” to exchange their current notes for ones that are all first-lien. This is good for the current second-lien holders involved as they move up in line in case One Call gets into financial difficulty in the future.

Debt holders were asked to trade $258 million in current notes for $235 million in new notes, which implies the current notes are discounted by 9 percent. (We don’t know if the original debt offering

had a similar discount.)

This closed, so this part of the effort is complete.

Part Two

One Call is offering to exchange up to $400 million in current term loans – some of which come due next year, others in 2022 – for new notes that mature in 2024. As of yesterday, about $103 million of debt has been committed to the swap.

Allow me to explain some terms.

·“first lien” debt is primary; that is, the entities that hold this debt get first dibs on assets in the event the debt issuer gets into financial trouble.

·“second lien” debt is next in line – a riskier position. If a company defaults, there may not be assets left so this type of debt usually pays a higher interest rate to compensate the debt holder for the greater risk.

·“notes”, “loans” or “debt” are all terms referring to a transaction where the creditor lends money to a debtor, and gets paid interest by the debtor. Mortgages and car loans are examples.

·“Payment In Kind toggle” notes allow the issuer to forgo interest payments by giving debt holders more first-lien notes instead

of paying the interest due in cash.

In other One Call news, Chief Strategy Officer Pat Rowland departed a couple weeks ago, and a few other folks have left as well. I continue to ping One Call to get their comments; just got a response from One Call that didn’t even bother to answer the key question; why was the initial debt swap cancelled.

If One Call decides to respond meaningfully I’ll update the post.

Don’t hold your breath…

Kudos to One Call and its bankers for moving to enhance its future cash position. This will allow the company to reduce cash payments to debtholders by something north of $20 million. Given the company’s most recent financials this is important indeed.

Posted by Joe Paduda on Wednesday, February 20th, 2019 | Comments

This week we are unpacking Single Payer/Medicare for All to better understand the many variations of SP/MFA and now they are different, how those variations might work, and whether some version is a) politically viable and b) would solve the cost/access/quality conundrum.

Can private insurers solve the healthcare cost problem? Well, on one level they get dinged if they control costs. A key point about for-profit insurers – the stock market loves and rewards revenue growth. In health insurance, revenue growth is overwhelmingly driven by higher medical costs. So, medical cost inflation = higher revenues = higher stock prices (yes, this is simplistic, but also mostly true).

Over the last two years insurers have kept premium increases low, but that’s due in large part to cost-shifting to members. In contrast, Medicare can’t cut costs by shifting them to you – benefits are set by law and rarely change significantly.

the big increase in Medicare 2000s was largely drive by the new Part D drug program; focus on per capita costs to account for changes in membership

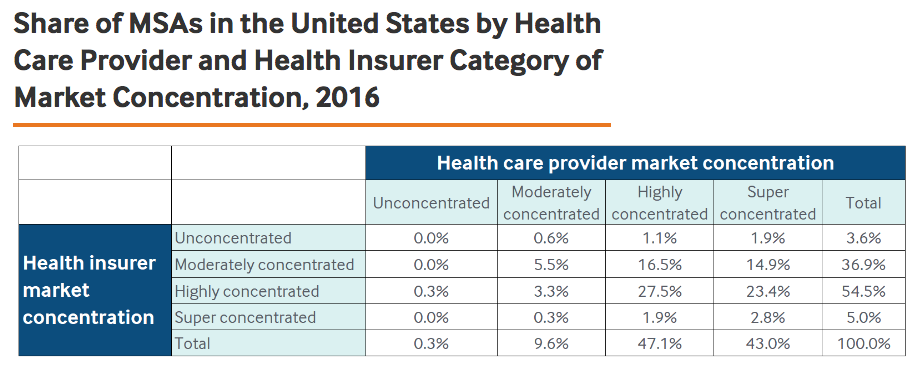

In 43% of markets, providers are super-concentrated, vs only 5% of markets for health insurers

That said, reality is health insurers have failed to control members’ healthcare costs. There are lots of reasons – including provider market consolidation, but as one of my rowing coaches once said to me; “I don’t want to hear why you can’t, I want to hear how you will”.

What does this mean for you?

If for-profit health insurers had done their job – controlling costs and delivering better outcomes and patient satisfaction – you wouldn’t be reading this.

Medicare has a better track record controlling cost – which is by far the most important issue in healthcare.

Tomorrow – can SP/MFA solve the cost problem going forward?

Note – Here are a couple approaches health insurers are working on, in process, have been tried, or may try in the future. In my view much of this is too little, too late.

Narrow networks – healthplans with very limited provider panels – are gaining traction as healthplans force providers to agree to lower prices and outcome standards in return for patient volume.

Posted by Joe Paduda on Tuesday, February 19th, 2019 | Comments

Word just in that One Call Care Management has “cancelled a bond exchange intended to rework its $2 billion debt load”. According to Bloomberg, OCCM won’t pursue the debt swap.

The swap would have allowed holders of the current second-lien notes to exchange some for first-lien notes. This would have moved the holders of first-lien notes up in the event there is a restructuring.

Don’t know if this will have any impact on the company’s ratings by Moody’s or Standard and Poor’s; will monitor and let you know.

Posted by Joe Paduda on Tuesday, February 19th, 2019 | Comments

It’s the worst kind of government over-reach.

It’s an easy solution to a huge problem that will cost nothing.

And everything in between. Between now and Election Day you are going to hear a lot about Medicare for All and Single Payer, and most of it will be utter nonsense.

So, this week is Single Payer/Medicare For All explanation week.

Proponents of Single Payer/Medicare for All say it will reduce overall costs and ensure everyone in America has great healthcare; At the other end of the spectrum, it’s fiercest opponents say it will bankrupt the country while giving bureaucrats control over your family’s healthcare.

Reality is, since there is no actual agreed-upon “Medicare for All” or Single Payer legislation, each of us sees what we want to see – MFA as the Holy Grail or a Total Disaster.

Let’s take a step back and think about how voters are affected by the core problem – or rather problems, with healthcare and health insurance.

The focus on voters is critical here – most are covered by employer-based health insurance, and most of the rest are covered by Medicare. For the non-elderly:

Health insurance is stupid expensive.

For many of us, deductibles are so high “insurance” just protects you from catastrophic injuries or illnesses.

Insurance companies control the doctors and hospitals you can use and the care you get.

The paperwork is mindboggling, confusing, and adds billions in unnecessary cost.

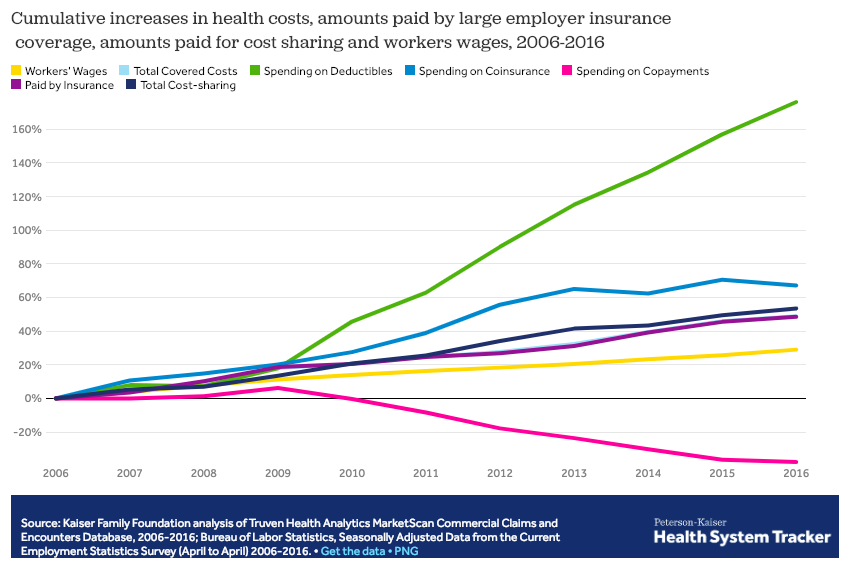

For workers, healthcare “costs” are a combination of insurance premiums and cost-sharing payments – mostly deductibles and copayments. (While about 75% of premiums are paid by employers, economists argue that most of those premium dollars would be paid in cash wages if health insurance wasn’t provided.)

Today family health insurance premiums are almost certainly more than $20,000 a year.

Over the last two decades, healthcare costs have eaten up wage increases – one of the main reasons families aren’t getting ahead.

For those who actually have to use their health insurance, it’s worse. Deductibles are so high that many families can’t afford them.

From S&P – “An obligor rated ‘CC’ is currently highly vulnerable. The ‘CC’ rating is used when a default has not yet occurred but S&P Global Ratings expects default to be a virtual certainty, regardless of the anticipated time to default.”

Posted by Joe Paduda on Thursday, February 14th, 2019 | Comments

There’s so much great research published every day – and a lot of crap too – that it is impossible to figure out A) what should I read and B) what does it mean.

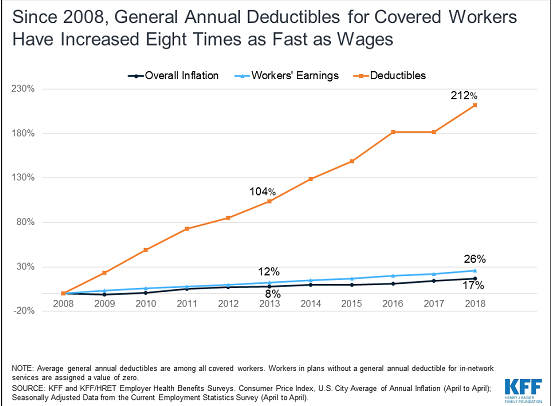

Of course, it’s not so much if you have insurance – it’s how much you have to pay out of pocket. Which, to coin a phrase, is becoming a ship-load as deductibles have exploded. Total worker cost sharing has increased about 50% over the last decade.

Posted by Joe Paduda on Wednesday, February 13th, 2019 | Comments

Yesterday’s post covered why work comp is a soft target for “revenue maximizers” – particularly facilities. Today we’ll talk solutions.

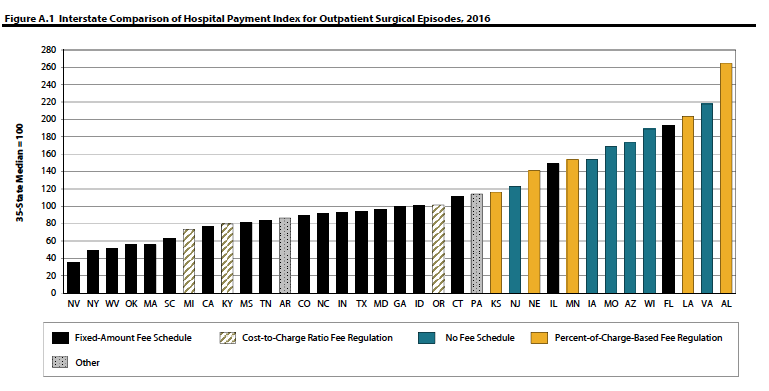

First, on a macro level, states need to develop and use fee schedules based on Medicare. For inpatient that’s MS-DRGs – and there should be no outlier provisions. A number of states do just that, and their facility costs are pretty much under control. WCRI has an excellent compendium of state fee schedules etc here.

Here’s one chart that shows how effective flat-rate fee schedules are at controlling costs (credit to WCRI’s Olesya Fomenko and Rui Yang)

there’s a lot more to this – see https://www.wcrinet.org/reports/hospital-outpatient-payment-index-interstate-variations-and-policy-analysis-7th-edition

Second, on a pre-claim level, payers should analyze hospitals’ and health systems’ actual paid amounts to determine what their costs are. Not the discount, the net cost.

Researchers will most likely find net costs are lower for not-for-profit healthcare systems/hospitals, regardless of the discount level. That’s because many for-profits have really high chargemaster prices that they then “discount” so payers can show a lot of “savings.”

Then, wherever and whenever possible direct patients to those lower cost facilities that have equal or better outcomes.

Third, the services have been rendered and a bill for a gazillion dollars appears.

Briefly, unlike group health and Medicare/Medicaid, many work comp payers don’t do much more than apply fee schedules, rules, some clinical edits and check for UR compliance, and perhaps do pre-payment audits. In the Medicare/medicaid/group health world there are both pre- and post-payment approaches, generally known as “payment integrity.”

Dr Pelezo: [a] key difference between group health (commercial), Medicare and Medicaid versus Worker’s Compensation involves the number of layers of payment integrity, the type of integrity, and the way those layers are implemented. In group health programs we have the core processing platform plus the implementation of at least one if not two large-scale industry editing software packages, and in some cases additional pre-payment fraud, waste and abuse software.

…there may be three or four payment integrity companies scrubbing the same bill set after payment has been made, each finding something that the prior vendor did not detect. In total you may have six or seven layers of protection in place. These key observations served as the impetus for Equian’s formation of a seamless second pass editing solution targeted specifically to Worker’s Compensation programs, one that would impact bill processing in all States. Remember, these are industry leaders in payment integrity – and this speaks to how difficult it is for any single entity or organization to detect ‘all’ improper payments, and frankly how much overpayment is present in any given environment.

I asked Dr Pelezo what payment integrity is and how it is different from bill review:

Dr Pelezo: In its simplest form payment integrity is payment to the right party, for the right medical products and services, in the right amount. In different forms every healthcare payer in the industry deploys various degrees of payment integrity – a worker’s compensation bill review engine in and of itself is a form of payment integrity.

Dr Pelezo: many worker’s compensation carriers are dependent upon bill processing systems and limited internal resources to manage the entire spectrum of payment integrity…the expertise, tools, and funding required to implement effective programs for all aspects of payment integrity is a daunting task (and a daunting ask). Even one ‘simple’ aspect of payment integrity (nothing here is simple) – bill auditing – can be subdivided into professional, outpatient, inpatient, pharmacy, durable medical equipment and supplies, etc. Securing true expertise in each of these individual areas can be difficult. Compound that issue with an ever-changing landscape of payment policies and methodologies and it is easy to see why managing payments is challenging for even the largest healthcare organizations. In bill auditing alone, one has to tackle validating/aligning new State requirements with bill processing outputs, CPT code updates, AMA CPT Assistant code clarifications, evolving specialty society guidance, National Correct Coding Initiative policy updates, hundreds of pages of CMS final rulings that impact CMS-based payment methods, medical policy updates, bulletins and banners, and all other information and reference material that impact how payment should be made.

What are some of the issues you’ve seen with outpatient services?

Dr Pelezo: I continue to see an expansion in billed amounts for outpatient surgical services, especially in those States that pay for services based on ‘usual and customary’ or percent of charge methods. Programs that participate in Medicare should not bill other payers differently than Medicare is billed for the same set of services, from a pure compliance perspective. I’m not convinced this is always the case, however, and I have encountered these variations in Worker’s Compensation data. I’m disappointed when I encounter an ambulatory surgical center bill for hundreds of thousands of dollars for surgeries that last a couple of hours; surgeries that under other programs – lock, stock, and barrel – are only reimbursed a very small fraction of the reimbursement received under Worker’s Compensation. [emphasis added]

What does this mean for you?

One of the fun things about working in this business is finding people like Dr Pelezo whose depth of knowledge and level of expertise reminds me that there’s always a lot more to know – and a lot more we can do.

A national consulting firm specializing in managed care for workers’ compensation, group health and auto, and health care cost containment. We serve insurers, employers and health care providers.