B2B sales is NOT about “value”, RoI, relationships, or anything else you think it is.

It is about meeting the emotional/psychological needs of the key buyers.

You may have sensed this, or interpreted it as “relationships” that make deals happen – but that is a misread. The reason relationships work is they reflect the sales person’s deep investment in getting to know the buyer(s), understanding what drives them (outside of obvious business goals), and mitigating their fears.

A terrific piece in Harvard Business Review speaks directly to this…(quotes from the article)

- findings indicate that B2B customers prefer interactions that fuel their psychological needs — even if they require more time or cost more money.

- Among vendors who provide “poor” service, only 33% of respondents reported that the vendor knows them personally. In contrast, among vendors who provide “good” service, respondents indicated the vendor knows them personally more than twice as often (70%).

- Even when you have an effective solution in mind, provide your clients with options so they’re reminded that they’re in control.

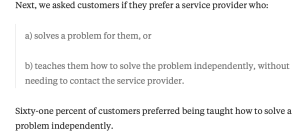

(this is directly supported by our most recent survey of prescription drug management in workers’ comp…respondents overwhelmingly want PBMs to provide them insight so they can fix problems collaboratively)- Our study also included some interesting findings around empathy. Expressing empathy, a common way of increasing connection with our friends and family, can backfire if customers perceive it to be disingenuous. Too often, service providers script empathy into customer interaction, assuming it’s what customers want to hear. That’s a mistake. Our research indicates that customers far prefer a service provider who responds knowledgeably over one who “feels their pain.”

What does this mean for you?

be genuine.

ask questions, don’t present.

don’t schmooze.