mostly because insurers and employers have a been asleep at the switch.

Republishing a post with minor edits from two years ago…LOTS more on the sleazy business of physician dispensing here…

WCRI’s latest report finds:

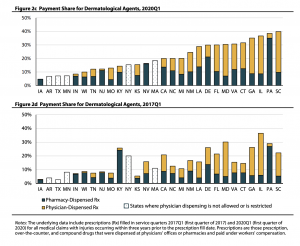

- Physician-dispensed drugs (PDDs) accounted for more than half of drug costs per claim in Q1 2020 in four states – Florida, Georgia, Illinois, and Maryland.

- In 12 states, doc-dispensed dermatological agents accounted for most payments for this drug class.

- Louisiana is worst-off, with employers paying $190 per claim for dermo drugs in the 1st quarter of 2020…Illinois is right behind at $181.

- Kansas and Connecticut saw payments for those dermo drugs triple from Q1 2017 to Q1 2020.

That profit-sucking prescribing by docs in Connecticut is why total drug spend increased 30% in the Nutmeg State – making it one of two states that had drug spend increases. Florida – the home state of PDD – was the other. (Across all subject states, drug costs dropped 41%.)

Having lived in CT for over 20 years, I’m really stumped by the precipitous increase in skin care drugs.

What could POSSIBLY be driving this massive need for occupationally-driven skin care/topicals?

- Did sun spots create a pandemic of skin cancer but somehow only affect the second-smallest state?

- Did a massive refinery accident expose tens of thousands of workers to burns or skin infections?

- Did a hyper-virulent new breed of poison ivy run rampant, affecting thousands of landscaping and municipal workers?

- Did the emerging cannabis industry fail to protect its workers from fertilizer burns, exposing thousands of workers to painful blisters?

- Did everyone in Connecticut suddenly become unable to swallow a pill?

Of course not.

The real question is this:

why haven’t insurers, TPAs, and self-insured employers used CT’s Medical Care Plan to ban physician dispensing? Payers including the Workers’ Comp Trust of CT have pretty much eliminated physician dispensing.

It’s not just Connecticut. PDD costs are outrageous, and all credible research indicates PDD is totally unnecessary, increases medical costs, and prolongs disability.

WCRI’s research should be a call to action. Legislators, regulators, and payers are doing their policyholders and clients a disservice by failing to aggressively attack physician dispensing.

And those clients and policyholders are equally at fault – it is up to you to work with your PBM and payer to stop this rampant profiteering.

What does this mean for you?

Yeah, I know it’s hard.

Stop whining and get serious.