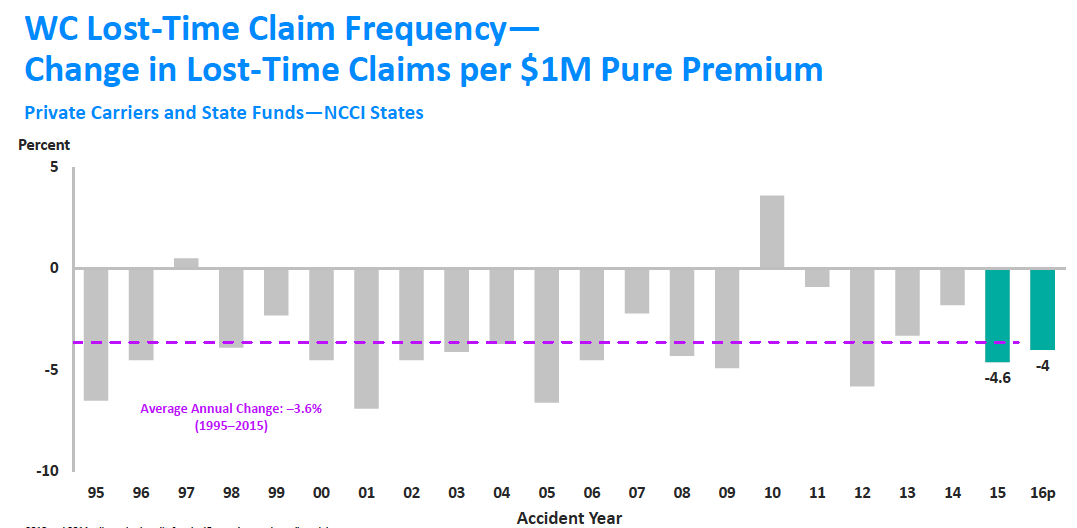

A few weeks ago I had the opportunity to virtually sit down with Coventry’s product development folks to hear what they’ve been doing with tele-.

I checked in again this week, and here’s what they’ve been up to. Quick take – tele-triage is gaining traction, while patients are slower to agree to do virtual office visits.

Coventry, a provider of services ranging from networks to pharmacy benefit management, case management to durable medical equipment, is well into Phase One, of their telemedicine offering which is tied into Coventry’s Nurse Triage program, NT24.

Working with technology vendor KuraMD Coventry’s nurse triage staff connects with the patient, evaluates the injury or illness, and, based on their findings, recommends an appropriate level of care whether it be self-care, a “live” visit with a clinician, or a telemedicine visit (urgent and emergent cases are identified at call onset). Diagnosis and other factors drive the recommendation.

While the program has been in place for the better part of a year, Coventry has found many customers have yet to embrace the telemedicine office visit. Customers have “a tough time thinking of this as an office visit.” Telemedicine providers provide initial visits where they can send patients to physical locations for physical therapy or for imaging studies. While TM follow-up visits are offered, to date most employers want patients to visit a provider for those follow-up visits.

The program is live with two TPAs; a total of 10 employers have been implemented to date nationally with 4 in single states. Employers are quite diverse, including labor, retail, temp staffing, and construction.

For those patients able and willing to use telemedicine for a virtual initial visit, Coventry uses providers contracted with KuraMD. Care coordinators initiate the tele-visit, ensuring the patient has the right technology, walking the patient through the set-up and sign-on process, then passing the patient to the clinician for the visit.

Concentra will also be working with Coventry in the future

Phase Two involves broadening the number of clinicians that can provide telemedicine and also offering telemedicine visits without the nurse triage component. As one of, if not the largest workers’ comp PPOs, Coventry is working to get information to the company’s contracted network physicians to educate them about the service and requirements, discuss compensation, and provide training. The credentialing process and standards are identical to the company’s “regular” network but there are more questions regarding state licensing to ensure compliance with state regulations.

Down the road, Coventry is looking to incorporate tele- into case management. Ideally, case managers would connect with the patient, provider, and/or employer via video conference and enter information in real-time into the company’s proprietary CM IT system. There’s much work to be done connecting with claims systems to identify the types of and format of information needed by adjusters, build data feeds, and separate out key bits of data that need an adjuster’s attention.

What does this mean for you?

Expect tele-visits to gain traction as patients use similar services for family members and their own care. Telemedicine is moving quickly in group health, and this will accelerate adoption in comp.

Clearly not a self-portrait; I could never grow that facial hair…

Clearly not a self-portrait; I could never grow that facial hair…