Another whirlwind week is just about over, and with it the summer of 2020.

Here’s important/interesting news that came across my virtual desktop this week.

COVID and Comp

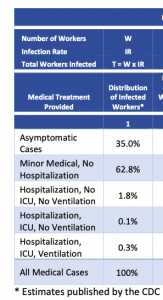

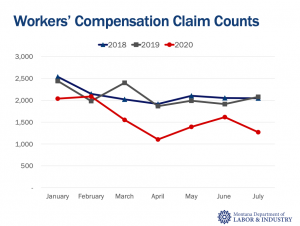

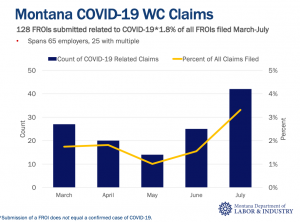

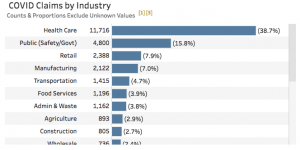

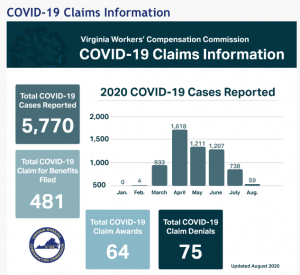

More data on workers’ comp COVID19 claims is coming in; Virginia’s Workers’ Comp Commission has published data; key takeaway is to date, only 8.3% of COVID19 claims reported have resulted in benefit payments. That will certainly increase as claims develop.

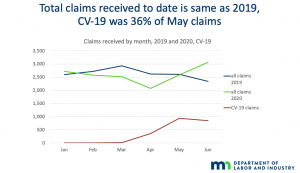

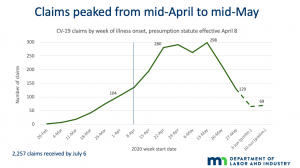

More info on state COVID reporting is here – you can watch a recorded webinar on the subject here – Mark Priven and I dive into data from California and Florida and discuss the implications thereof.

Meanwhile, employment took another hit as last week more than a million Americans filed for unemployment. This continues a five-month run of claims at or above the million mark. 14 million of us are still without jobs.

COVID19’s impact on health insurance coverage

Several million people have lost their health insurance due to COVID19-related job losses. We don’t know the specific number – and it is certainly increasing – but it is likely between 3 and 12 million. (download the report for details).

Another perspective is here.

Most of those folks are lower-income workers and many are minorities; some may be eligible for Medicaid however states that did NOT expand Medicaid such as Texas and Florida will see an increase in uninsured care costs.

Congratulations to myMatrixx and new Chief Sales Officer David Dubrof; David is one of the very few “A” players in work comp services sales; myMatrixx will benefit greatly from his sales leadership. David and his colleagues are equally fortunate; payers have consistently rated myMatrixx the top workers’ comp PBM. (myMatrixx is a client)

NCCI published a report on the impact of fee schedule changes on outpatient facility costs. Good to see this rapidly-rising cost driver getting attention.

Implications

- Fewer jobs = lower payroll = lower work comp premiums

- Things are tough and getting tougher for lower-wage workers, which are disproportionally people of color.

- More uninsured = more need for facilities to get $$ from those who are insured.