This was the message Accident Fund’s Jeff White delivered in a recent presentation on disruption in insurance – and specifically workers’ comp. A few of Jeff’s slides are shared here…

The idea is simple – things you used to have to do via phone or fax or in person or thru the (gasp) snail mail you can do on your smartphone or tablet – instantly, securely, and at no cost.

Hotel reservation? Hotels Tonite.

Plane? Get a reservation, get flight status pushed to you, change your seat, get an upgrade.

Get dog food? Amazon Prime.

Nearest coffee? Starbucks app – and pay for it too.

Check on your house? Sure – lock status, turn up the heat, watch home security cameras.

Banking? Deposit checks, pay bills, move money around via your phone.

Sports? Get scores, watch highlights, chat with fellow fans, post pictures, buy tickets.

Travel, retail, security, banking, entertainment – all have been disrupted, middlemen eliminated or drastically changed by adoption of smartphones, spread of a very fast internet, growth of artificial intelligence-driven decision making, internet banking.

This is happening with insurance now, driven by those same technologies, processes, capabilities. Think about the implications; here’s one.

Insurance is risk-sharing for potential losses, but it is a very blunt instrument. Risk is estimated using what are really crude tools to assess exposure, potential cost, liability. Technology allows risk takers and risk assumers to narrow down the actual “risk” a lot, lowering cost of risk and more accurately pricing that risk. Others with similar risks share the burden – but that burden is much lower due to accurate understanding of exposure.

If a loss occurs, tech can pay the claim instantly.

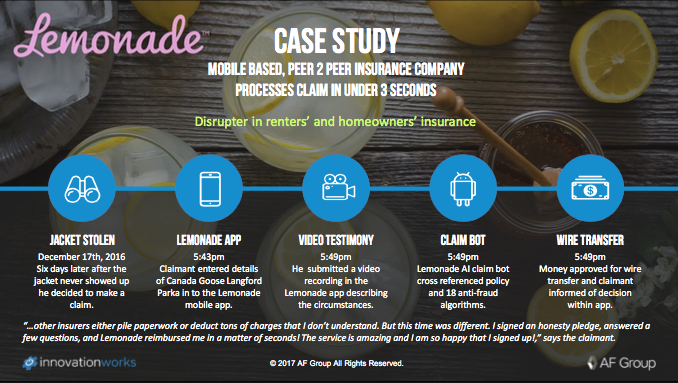

The graphic below is not a “could be”, it’s a “what actually happened in real life.”

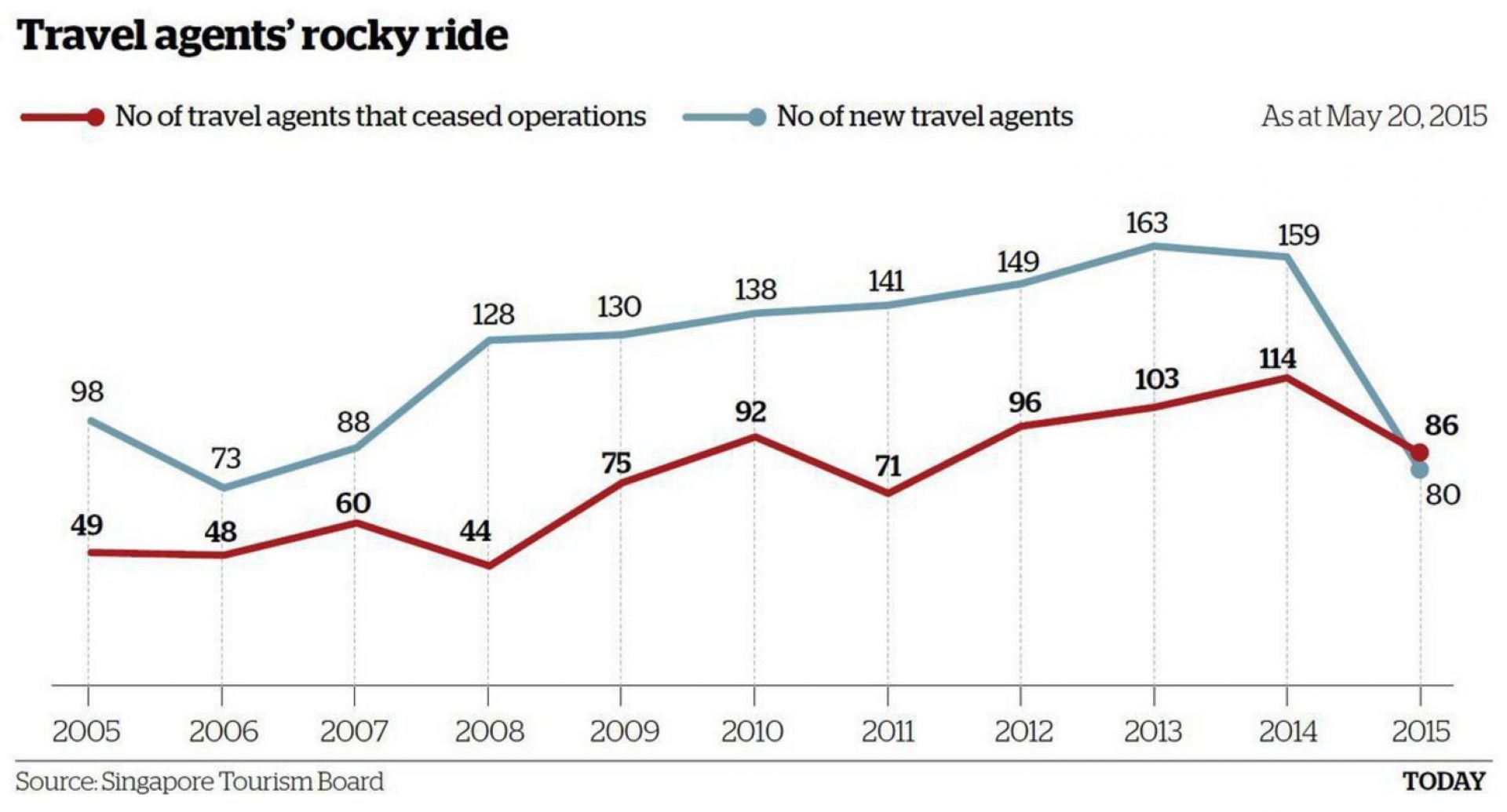

Think this won’t happen in workers’ comp?

Ask a former travel agent – there are lots of them.

Most insurance companies will NOT survive the transition. That’s because they don’t want it to happen as it will reduce revenues, eliminate the need for executives with newly-irrelevant skills and experience, and make existing infrastructure partially obsolete.

New entrants who don’t have lots of infrastructure to support and business models rooted in current technology and buying patterns are the “Ignorant Antagonists”. Many of them will fail due to “stupid, ignorant” mistakes – but some will survive, thrive, and come to dominate the insurance industry.

What does this mean for you?

Your company tomorrow will be a lot different than it is today. If it is around tomorrow.

Ah, it’s easy to envision the eye-rolls from this post, Joe.

Nobody likes to hear that the sky is falling but what if it REALLY IS this time?

I’ll go on the record NOW and say that the future will belong to those who make things better, faster, and SIGNIFICANTLY cheaper. The fact is that insurance is among the lowest-hanging of fruits to technology entrepreneurs. Disintermediation is all but guaranteed in the years ahead and consumer costs are poised to DROP. Yup; I’ll say the same about healthcare costs too!

Oh, and for c-suite executives who are comforted by the prospect that ‘regulations’ will prevent new technology-driven business models from gaining a foothold any time soon, please note that the same thinking didn’t stop self-driving cars from hitting the roads FASTER than anyone predicted…the entire U.S. auto industry is now at risk for bankruptcy (except for Ford, maybe) because of technologies developed by Google, Uber, and Tesla.

The reality is that innovators from outside of the insurance industry are more than willing to ask for forgiveness rather than permission in pursuit of their solutions. They are also willing to take risks and to even fail sometimes. By contrast, the insurance industry is dominated by professionals who are often RISK ADVERSE. This is NOT the time to double-down on improving the quality of your horse drawn carriages, folks…you must embrace (or buy) that which makes your old model obsolete if you want to survive.

Jeff White has pulled the proverbial fire alarm and I couldn’t agree more! Sadly, it will be largely ignored. So be it; there’s a whole new generation of leaders who see the world very differently and are eager to fill the void that is left behind…very soon.

So true!

Good insight Joe. I work for a technology company offering a telemedicine solution specific to workers comp (CHC) and just recently used telemedicine for the first time for my own personal needs. It saved me so much time and hassle…15 minutes vs. 2+ hours! Companies that embrace new technology like telehealth in workers compensation will be rewarded.