A couple years ago, we heard endless stories about how “Obamacare” premiums were shooting up, individual health insurance was unaffordable, and families were going bare because the morons that came up with the ACA screwed it up.

Now, with average premiums up 30 percent, we hear…crickets.

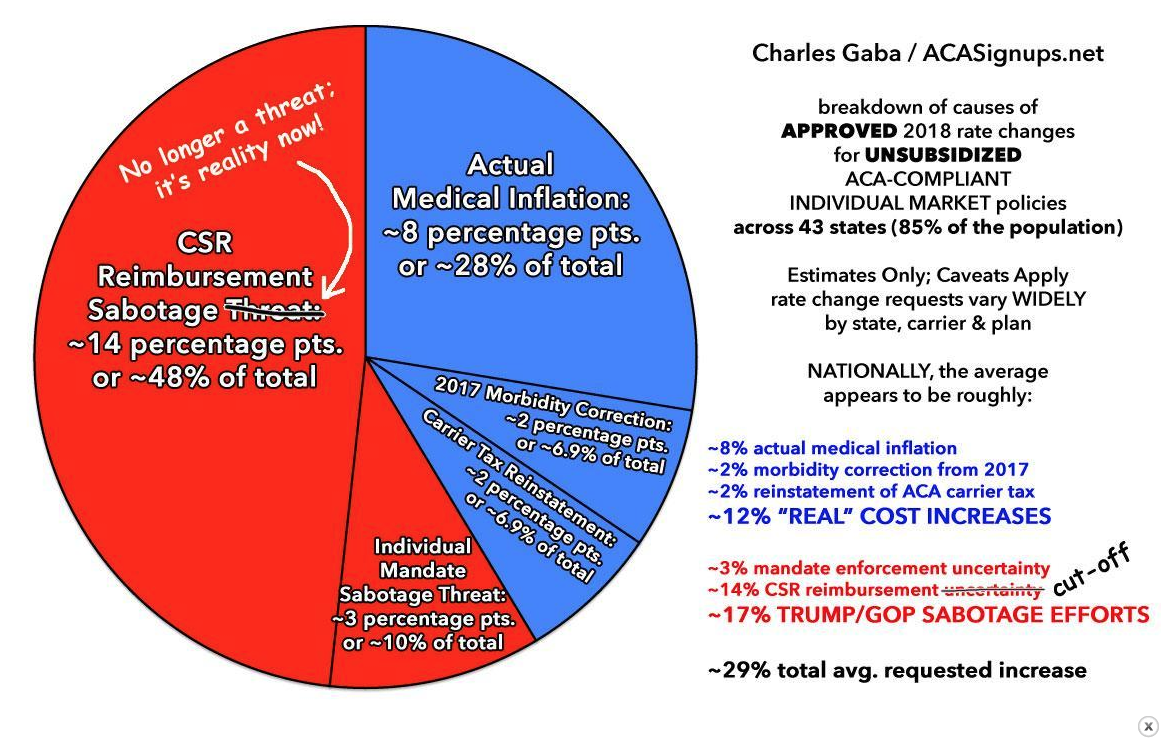

The reason premiums have gone up by about a third is simple; President Trump stopped the payments that subsidized low-income folks and insurers are scared he’ll stop enforcing the individual mandate. Unsurprisingly, many people dropped coverage, and insurers had to raise premiums because their risk pools worsened.

Chart credit Charles Gaba, ACASignups.net

If CSR payments were still in place, and insurers assured the mandate would be enforced, premium increases would be less than half they are today.

What’s scary about this is how easily the media’s focus is influenced by outside efforts. Instead of informing us of this very real, and very important issue, the media is all wrapped up in arming teachers, death penalties for drug dealers, and Stormy Daniels.

What does this mean for you?

A reminder that all of us have to stay focused on the important stuff, not the shiny objects.

Joe while that may be a factor the big driver is Hospital consolidation . In addition they are buy physicians, free standing facilities and other assets that threaten their empires.

The recent moves by CVS/Aetna and United being the largest owner of provider practices in the country is to fight the evil empires the hospitals have created. In NY most hide behind the “Not for Profit” status as the record record surpluses.

Joe

No question provider consolidation is a cost driver. The research clearly indicates consolidated areas have higher medical prices and costs.

Completely agree with this article! DRW

You are absolutely correct Joe. Health Insurance is really getting important nowadays. If CSR payments were still in place, and insurers assured the mandate would be enforced, premium increases would be less than half they are today. We need to take care of that. Great Information! Thank you

Joe – What are your thoughts on Idaho’s move to offer a cheaper, stripped down version of the ACA’s health coverage?

https://www.nytimes.com/2018/03/09/us/idaho-health-insurance.html

Hi Brad – thanks for the question.

There are two core problems with those plans. First, they typically don’t cover the really expensive care folks may need due to accidents, cancer, cardiac illness etc. and/or restrict providers that are covered. So, if you REALLY need care, you may well be on your own.

Second, healthier people preferentially buy these plans, leaving older and sicker people in the regular plans. This increases premiums for the regular plans, starting the downward cycle driven by adverse selection.

I’d also note that these have been tried and failed dozens of times in the past; I recall many instances of angry policyholders furious when their “plan” turned out to be insurance in name only.

So, I’m not a fan.